Home Insurance Is Disappearing; Climate Change Is the Reason

By Riley Monroe. May 31, 2026

The Coverage Crisis

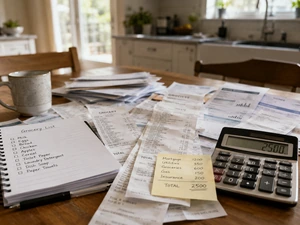

For millions of American homeowners, a seemingly stable asset-their house-is becoming harder to insure. Major insurance companies including State Farm, Allstate, and Farmers Insurance have stopped writing new policies in California and Florida. Some have exited these markets entirely. Homeowners are being dropped from coverage, facing astronomical rate increases, or turned away when seeking policies. The culprit: rising climate risk that has fundamentally changed how the insurance industry calculates risk.

According to the Levy Economics Institute’s April 2026 analysis of the homeowner insurance crisis, the situation represents a rapid destabilization of the U.S. insurance market. Climate-related natural disasters-hurricanes, wildfires, floods, tornadoes, and severe weather-are occurring with increasing frequency and severity, straining insurers’ ability to maintain profitability in high-risk areas.

The Numbers Behind the Crisis

The scale is massive. According to the Levy Economics Institute report, in 2022 alone, 1 in 6 homeowner’s policies were cancelled nationwide due to rising hurricane risks. In Florida, 12 home insurers exited the market or suspended new policy offerings in 2022. By 2023, Farmers Insurance pulled out of Florida entirely, leaving 100,000 customers without coverage. In California, seven major carriers have either left the market or reduced coverage since 2022, according to reporting from the California Public Policy Institute.

The financial pressure is real. According to Change The Chamber’s March 2026 analysis, home insurance premiums in the United States surged by roughly 30 percent between 2021 and 2024-significantly outpacing inflation. In Florida, homeowners pay the highest rates in the nation, averaging $15,000 annually for homeowners insurance. Some homeowners are now paying more for insurance than for their mortgages.

State-by-State Emergency

Florida and California have been hit hardest, but the crisis is spreading. According to the Center for American Progress, insured losses in the United States reached $112.7 billion in 2024-a 36 percent increase over the prior year. In California, a one-year moratorium on insurance cancellations in wildfire-disaster areas is scheduled to expire in January 2026, expected to accelerate further coverage losses.

California’s FAIR Plan-an insurer of last resort-has seen its exposure more than double in less than two years to $650 billion, according to recent reporting. This is creating systemic concerns about whether state backup systems can absorb further market withdrawals. Florida’s similar Citizens Property Insurance Corporation has grown to over 1.4 million policies, far exceeding historical levels.

The Ripple Effect

The insurance crisis is now disrupting home sales. According to real estate industry reporting from October 2025, 13 percent of California realtors reported that at least one sale fell through because buyers could not secure homeowners insurance-nearly double the rate of the prior year. This scenario is expected to become more common as moratoriums expire and more insurers withdraw.

For some homeowners, the crisis is becoming unmanageable. According to reporting on the situation, as insurance becomes increasingly out of reach, some homeowners are forgoing insurance coverage entirely-a dangerous choice that exposes them to catastrophic financial risk. Others are being dropped and relying on state-based insurers of last resort, which typically offer less favorable coverage terms and higher premiums.

Why This Is Happening

The cause is straightforward: climate science. The January 2025 California wildfires caused approximately $250 billion in damage, with insurers expected to pay out $40 billion-the largest wildfire insurance payout in history. Scientists estimate that climate change increased the likelihood of those fires by about 35 percent.

This is not a temporary problem. According to multiple analyses of climate trends, extreme weather events and natural disasters are projected to grow in frequency and severity. Traditional insurance models-which rely on historical risk data to price premiums-are fundamentally incompatible with rapidly changing climate patterns. Insurers are withdrawing not out of greed, but because their actuarial models suggest that high-risk areas will generate unsustainable claims in the coming years.

The Housing Affordability Question

As insurance costs soar and availability shrinks, the broader housing crisis deepens. Lenders require homeowners insurance before approving mortgages. Without available insurance, homes become difficult or impossible to finance. This is beginning to restrict who can buy homes in climate-vulnerable areas, potentially reshaping real estate markets across the country.

For now, there’s no clear solution. Rate regulation in California has prevented premium growth but may have accelerated insurer withdrawal. Florida’s deregulation has allowed higher premiums but hasn’t prevented market exits. Federal intervention, disaster relief programs, and innovative risk-sharing models have been proposed, but implementation remains limited. For homeowners in high-risk areas, the message is clear: the cost of climate change is no longer a future problem-it’s reshaping the economics of homeownership right now.

References: Harvard Business School: Climate Change Upending Homeowners Insurance | Real Estate News: Insurance Challenges Impact Future of Home Sales | Levy Institute: A Premium Crisis

The News Command team was assisted by generative AI technology in creating this content

Trending

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More

Read More